OCTOBER 23, 2010 – In uncertain times, the headline was soothing – “Secretary Geithner vows not to devalue dollar.”[1] United States Secretary of the Treasury Timothy Geithner was saying, in other words, that if there were to be “currency wars” – competitive devaluations by major economies in attempts to gain trade advantage with their rivals – the United States would not be to blame. Who, then, would be the villain? China, of course. Earlier this year, Democratic Party congressman Tim Murphy sponsored a bill authorizing the United States to impose duties on Chinese imports, made too inexpensive (according to Murphy and most other commentators) by an artificially devalued Chinese currency. “It’s time to deliver a strong message to Beijing on behalf of American manufacturing: Congress will do whatever it takes to protect American jobs.”[2] But the Geithner balm and the Murphy hyperbole are simply matching sides of a deep hypocrisy. For three generations, the United States has leveraged its position as the centre of empire to print dollars with abandon, devalue at will, and “debase” its currency at a rate impossible for any other economy. But the privileges of empire are starting to unravel, and the U.S. economy is wallowing in the consequences of 60 years of irresponsible monetary policy. Emotional attacks on China are simply a cover for problems deeply rooted in the U.S. itself. One part of that is a long history of currency wars, where the U.S. dollar has been used as a weapon in a manner without parallel in the modern world economy. That story has four aspects – Bretton Woods; the Nixon Shock of 1971; Petrodollars; and Quantitative Easing. This article will look at each in turn.

1. “Good as Gold” at Bretton Woods

To get to the first aspect of this story, you have to dial the film back to the restructuring of the world economy out of the ruins of the Second World War. In 1944, as that catastrophe was winding to a close, representatives of 44 allied nations met in Bretton Woods, New Hampshire to try to develop policies to prevent history repeating itself. Prior to 1914, capitalism had by and large been able to develop through exporting its horrors to the Global South – bringing genocide, slavery and the destruction of ancient civilizations to the Americas, Africa and Asia. But from 1914 on, some of those horrors had come home to the heart of the system itself. World wars engulfed the most “civilized” and capitalist powers themselves, first from 1914 to 1918, and then again from 1939 to 1945. Between these two moments of industrialized slaughter was the interlude of the Great Depression – the unprecedented collapse of trade, finance, employment and income, which shattered lives for a decade. It was clear to everyone that these two elements – war and economic collapse – were intimately related, and that to forestall another military catastrophe, deep economic restructuring would be required.

In this context, a once obscure economist emerged into prominence. In 1919, the then 30-something John Maynard Keynes was horrified when the peace treaty imposed by the victorious allies – the Treaty of Versailles – put in place punitive reparations on Germany. Keynes argued that the billions of dollars that were to be stripped out of German society would impoverish and embitter the country, lay the ground for economic difficulties, and for new wars. He captured this in his first major book, The Economic Consequences of the Peace.[3]

By 1944, Keynes was no longer an outsider and critic. This time he was at the table – one of the chief architects of the Bretton Woods’ institutions which were to emerge from this gathering. His ideas were listened to, in part because his warnings in 1919 had been so appallingly confirmed. His argument that economic competition needed to be regulated, that there had to be a central role for the state to mitigate the effects of the boom-bust cycle, and that there had to be institutions which could manage competition at an international level – these ideas were to be taken very seriously, as policy makers everywhere stared back at the horrors which were the alternative.

The Bretton Woods discussions would create the International Monetary Fund (IMF – designed to “administer the international monetary system”) and the International Bank for Reconstruction and Development or World Bank (“initially designed to provide loans for Europe’s post-war reconstruction”).[4]

But two other key goals were not achieved. One has been well-documented. Keynes had wanted an “International Trade Organization” to forestall the vicious trade wars which had broken out in the 1930s. He was not successful on that front. All that could be arrived at was the General Agreement on Tariffs and Trade (GATT), which took until 1995 to evolve from an agreement into an institution in the shape of the World Trade Organization (WTO). The second unrealized objective has received much less attention. It was to establish an “International Clearing Union” (ICU) for use in transactions between countries.[5] The U.S. – enthusiastic backer of much of the Bretton Woods’ discussions – was completely opposed to this. The establishment of an ICU would have sidelined the role of the U.S. dollar in international transactions. Emerging from the war controlling something like half of the world economy, the United States looked forward to the advantages that would accrue to its corporations and government from its new place as the centre of empire. Without an ICU, the U.S. dollar – like the British empire’s pound before it – would almost inevitably become the chief currency for international transactions.

Money is a peculiar thing. It is the necessary link between producers and consumers, employers and workers. It is also something that can be a “store of value.” Accumulate a lot of money, and you can have access to a lot of commodities, or a lot of that most special of commodities, labour power. In the early years of the world economy, precious metals, such as gold and silver, evolved into the material of choice to represent value – scarce enough to be “valuable” in themselves, but abundant enough so they could circulate in sufficient quantities to keep the economy functioning. In states that were sufficiently large and stable, a modification of this system developed. Paper money (probably first used in China more than 1,000 years ago) is essentially a promise that, should the holder so choose, the paper can be exchanged for a certain amount of gold or silver. So precious metals had not disappeared from the equation. They had simply been pushed into the background.

At Bretton Woods, the U.S. argued for and won a particular framework by which money could circulate in the world economy as a whole. It argued that it could guarantee currency stability by a double linkage – world currencies to the U.S. dollar, and the U.S. dollar to gold. Other currencies could price themselves in U.S. dollars, and that would be “good as gold” as the U.S. committed that anyone who wished, could turn in their U.S. dollars in exchange for the real thing – for gold, held at a fixed rate of $35 an ounce.

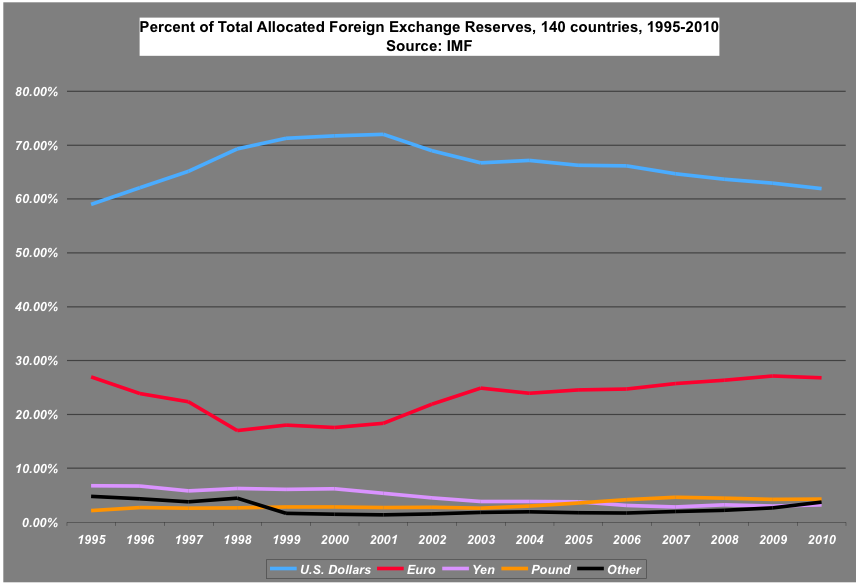

The establishment of the U.S. dollar as the world’s chief currency for international transactions had some risks. Should everyone with U.S. dollars demand they be exchanged for gold at the same time, the system would be in crisis. But it also held out enormous benefits. A key component of the world economy consists of the international reserves held by each country’s central bank to facilitate economic exchanges between nations. Traditionally, the key component of these reserves was gold. But with the U.S. dollar “good as gold” it became increasingly the practice for central banks to hold U.S. dollars as their international reserve, along with and increasingly in place of gold. The U.S. dollar was not the only such currency. Most central banks hold reserves in several of the different major currencies. But since Bretton Woods, by far the dominant currency held in central banks has been the U.S. dollar. Charts mentioned in this analysis are available at the end of the article. The first chart[6] shows that this remains true into the 21st century. At any one time between 1995 and the present, U.S. dollars represent some 60 to 70 per cent of allocated international reserve holdings throughout the world.[7]

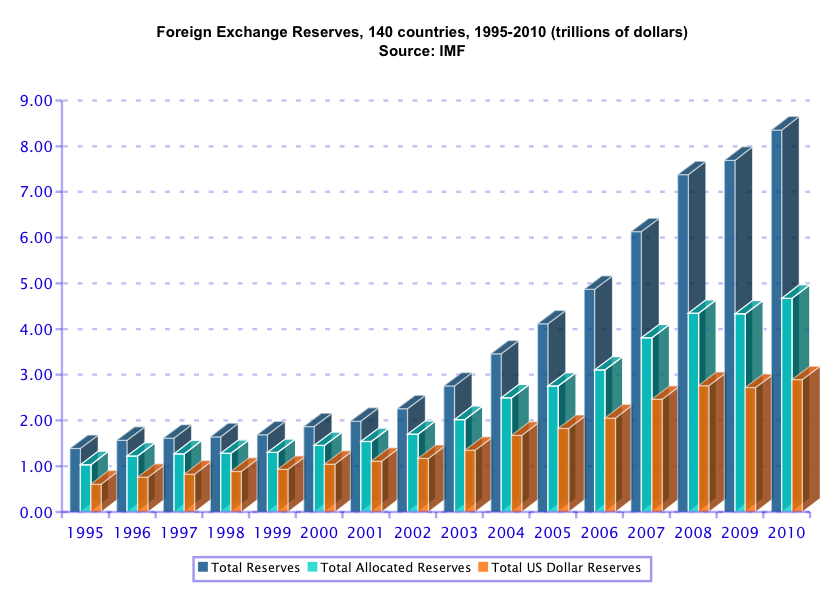

There are some important qualifications to be given to these percentages. First, these figures are provided “on a voluntary basis” from the 140 countries participating in the IMF process which compiles them. Second, not all international reserves are identified. The percentages here are for “allocated” reserves alone. There is a quite large, and growing, portion of international reserves held by central banks which are “unallocated” because the IMF simply does not know what they are. In 1995, 26 per cent of foreign exchange reserves went into this mystical “unallocated” category. By 2010, that had risen to 44 per cent. These qualifications aside, it remains the case that fulfilling the role of internationally recognized “store of value” for international transactions, requires a huge quantity of U.S. dollars, measured in the trillions. The next chart[8] demonstrates this, showing total foreign exchange reserves, total allocated reserves, and total reserves held in U.S. dollars. The amounts are vast (by 2010 more than $8 trillion in total foreign exchange reserves, of which more than $3 trillion in U.S. dollars) and growing.

This was the first, and centrally important, privilege of empire. The United States, alone in the world economy, had partially broken the link between trade deficits and currency decline. Most countries which run large trade deficits, see their currency decline in value. Less relative demand for an economy’s goods means, normally, less relative demand for that country’s currency. But the United States could partially defy that law. Regardless of demand for U.S. goods, there is always a demand for U.S. dollars, as the principle “store of value” for central banks around the world. As long as the U.S. dollar was “good as gold” it could run – and has run – very large trade deficits, without seeing its currency collapse. The annual trade deficits which the U.S. has been running since 1975 are a downward pull on the value of the U.S. dollar. But that has been significantly lessened by the constant demand for the U.S. dollar as a store of value on an international scale.

It is, then, of some interest, what exactly is represented by the large and growing “unallocated” portion of foreign reserves, pictured above. If that represents a hidden move away from the U.S. dollar towards other currencies, then this long love affair between the world’s central banks and the U.S. dollar might be in jeopardy. If and when that love affair ends, and the U.S. dollar starts behaving like a “normal” currency, the consequences will be profound.

2. The Nixon Shock and the Era of Devaluation

So the first, and still important, privilege of empire was to establish the U.S. dollar as “world money.”[9] But empires do not last forever. The second aspect of United States’ currency wars developed in the late 1960s and early 1970s, as the first signs of the relative weakening of the U.S. empire began to reveal themselves.

Part of the background were the U.S. wars in Indochina. From small beginnings under John F. Kennedy, these wars under first Lyndon Johnson and then Richard Nixon, grew into murderous, destructive and hugely expensive affairs. The U.S. had won the right, through Bretton Woods, to print money almost without impunity. But emphasis here has to be put on the word “almost.” The enormous expenses involved in keeping an army of half a million overseas began to put severe strains on the U.S. economy.

The other part of the background had to do with the defeated powers from World War II. Japan and Germany (and with Germany the rest of Europe) had considerably recovered from the destruction of war. Their economies were growing, and they were not burdened with the cost of empire and war as in the United States. Crucially, the recovering European and Japanese economies were running big trade surpluses, and accumulating growing piles of U.S. dollars. Gold on the open market was trading above $35, but the Bretton Woods’ exchange rate system pegged the U.S. dollar to gold at $35 an ounce. Increasingly, central banks, in Europe in particular, were exercising their Bretton Woods right to convert their U.S. dollars for gold – in effect, gaining access to gold below market value. The dangers to the U.S. economy were very clear, as gold fled the country both to pay for imperialist wars and to meet Bretton Woods obligations.

Secretary of the Treasury John Connally, a life-long militarist and hawk, would not, of course blame U.S. foreign policy adventures for the crisis of his country’s economy. But the other half of the equation he saw absolutely clearly. He argued that action was needed “to head off what the Administration believe[d] to be the most important non-military threat to U.S. national security: economic competition from Japan and Western Europe.”[10]

August 15, 1971, Richard Nixon announced a New Economic Policy. In Japan, it became known as the Nixon Shock. That day, the Bretton Woods system broke down. More accurately, the United States walked away from Bretton Woods. Nixon announced that the U.S. would no longer automatically exchange U.S. dollars for gold at $35 an ounce. In effect, he was removing gold as the standard by which currencies were measured, leading to the current system of “floating” exchange rates. The immediate effect was a steep and stunning decline in the value of the U.S. dollar relative to other currencies. This was precisely the intention of the Nixon Shock. As Time magazine reported in 1971: “American officials who once proclaimed the majesty of the dollar now cheer declines in its price on newly freed money markets, because they hold the potential for helping the U.S. balance of payments.”[11] This was devaluation on a scale about which China can only dream. And it is a devaluation which has continued in the almost forty years since.

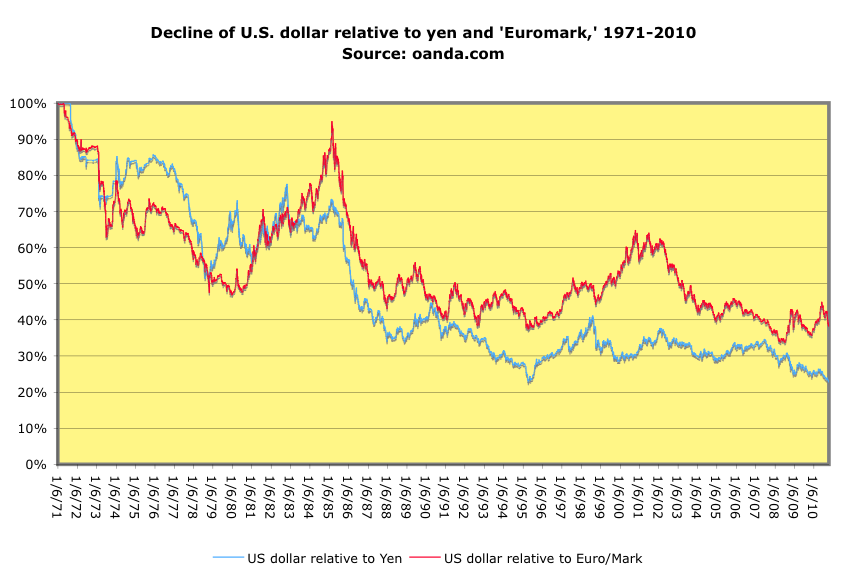

A previous article examined some of the statistical challenges in measuring the relative strength of the U.S. dollar.[12] The most common database by which to compare the relative strength of currencies begins in 1973. In other words, it excludes the impact of the Nixon Shock, and in doing so “flattens” the picture, showing only a modest downward trend for the U.S. dollar. But a database with a more complete set of statistics, stretching from just before the Nixon Shock to the present, can be put together from other sources – with figures for the U.S. dollar, the historically most important currency in Asia (the Japanese yen) and the “euromark” (a composite notional currency comprised of the German mark until 1998 and the euro from 1999 on). The result, visible in the third chart[13], is very clear. The U.S. dollar is approximately 1/3 of what it was in 1971, compared to the yen and the “euromark,” and its trajectory is without question down. The reasons for this long-term slide relative to other major currencies are for another paper. But the fact of the weakening of the U.S. dollar is incontrovertible.

It is worthwhile at this point in the analysis to marvel at the arrogance of U.S. policy makers. In 1944, a system to stabilize the world economy was put in place, which had the side benefit for the United States, of privileging its currency as the store of value for central banks around the world, allowing United States’ policy makers to print money almost at will. When this capacity to print money out of proportion to the needs of the economy, in particular to finance murderous wars in Indochina, started to put strains on the system, the United States simply walked away from its obligations. It left the Bretton Woods’ monetary system in ruins, and imposed on the rest of the world a remarkably steep devaluation of its currency, making U.S. produced goods more competitive, and those produced in Japan and Europe less so. We could end the story at this point. The evidence of U.S. manipulation of the world currency system to its advantage is overwhelming, and has a very impressive pedigree. But the story is only half done. There are two other key aspects to the “privilege of empire” still to be examined.

3. Petrodollars: the fuel of empire

The collapse of Bretton Woods led to a short-term devaluation of the US dollar. Other things being equal, it is conceivable that this devaluation could have accelerated into a collapse. However, the death of Bretton Woods was followed by another era in the history of the dollar – that of the Petrodollar. In the early 1970s, the Organization of Petroleum Exporting Countries (OPEC) made the historic decision to invoice the trade of oil in dollars. In part under the direction of then Secretary of State Henry Kissinger, the United States and Saudi Arabia in 1974 launched the “United States – Saudi Arabian Joint Commission on Economic Cooperation.” The key decision arising from this commission was for Saudi Arabia to sell its oil in U.S. dollars. “As the largest OPEC producer, the Saudis used their strong influence in OPEC to persuade other members to follow suit; and they did. In 1975, OPEC announced its decision to invoice oil sales in dollars.”[14]

This meant that there was another reason for every nation to hoard U.S. dollars, whether buying goods from the U.S. or not. To buy oil, you needed U.S. dollars, something which set both oil and the U.S. dollar apart from their equivalents in the world economy. To buy apples produced in Canada, someone outside of Canada in effect has to buy Canadian dollars at the same time. The apples are priced and traded in local (Canadian) currency, so a demand for apples implies a demand for the Canadian currency. But not with oil. To buy oil from Saudi Arabia – or Iran, or Venezuela – you didn’t need access to the currencies of those nations, but rather to U.S. dollars. Increasing demand for oil from these producers, then, meant perversely increasing demand for U.S. dollars. Bessma Momani summed it up as follows.

Since the mid-1970s, the value of the United States’ dollar has been upheld by a number of domestic and international factors. An often underestimated factor is that oil is sold and traded in US dollars. Arguably, having the dollar used as the ‘main invoice currency’ for oil makes the trade of this vital resource the new post-Bretton Woods’ Fort Knox guarantee of the dollar.[15]

Nixon broke the link with gold in 1971, and at first glance that should have led to a very steep and long term decline in demand for the U.S. dollar. But because of the pivotal role of the U.S. dollar in the international oil market – the market for the one indispensable commodity for world capitalism – the decline was mitigated. There remained constant demand for the U.S. dollar because of permanent and rising demand for oil.

The United States again benefited from the “privilege of empire.” They could slow the decline of the dollar because of their still dominant position in the world economy. With a resulting capacity to print dollars far in excess of that of other nations, the United States has been able to continue financing enormously expensive wars abroad, while at the same time running large and growing trade deficits at home. No other country in the world has this kind of capacity.

There were other perverse effects from the creation of a world awash in petrodollars. The oil exporting countries amassed huge quantities of these dollars, far in excess of anything they could spend internally. In the late 1970s and the early 1980s, much of these excess funds “were saved and deposited with banks in industrial countries,” in particular in banks in the United States. “The banks, in turn, lent on a large part of these funds to emerging economies, especially in Latin America. When the oil boom subsided in the early 1980s, bank flows to emerging markets reversed sharply, triggering the Latin American debt crisis.”[16]

That is how the antiseptic language of an IMF working paper outlines the issue. It could be restated as follows. Billions of dollars left the United States, Europe and Japan to pay for oil imports in the 1970s and 1980s. The billions of dollars received by OPEC countries were far in excess of any local consumption and development possibilities (in large part because these countries had distorted development patterns after decades of oppression by the rich countries of the Global North.) So in turn, these billions flowed back to the Global North in the form of massive deposits in particular into U.S., banks. “Nearly 500 billion petrodollars were recycled from oil producers with a capital surplus to countries with trade deficits.”[17]

It didn’t end there. The same processes driving this flow of money – the spike in the price of oil in the 1970s – made it very difficult for developing countries in Latin America to finance their industrialization. They had “balance of payments” problems. Under pressure from the IMF, these countries were encouraged to borrow the petrodollars sitting in the vaults of the Global North banks. These petrodollars were in effect ” ‘recycled’ through the IMF”[18] in the form of loans to countries in the Global South from the excess money sitting in the banks of the Global North. This was aggressively marketed as an alternative to the nationalism and state-led development strategies of the 1960s and early 1970s. When interest rates spiked in the 1980s, the loans incurred became unsustainable, and the economies of Latin America spiraled into a deep crisis.

Billions of dollars slosh through the world economy, enriching states and financial institutions in the Global North, creating short-term frenzies for debt-financed development, and laying the basis for long-term crisis in the developing world. The petrodollar aspect of U.S.-based currency wars is an issue for the poorest countries of the world, not just its richest.

The benefits of the Petrodollar era might be beginning to unravel for the United States. Bessma Momani concludes that it is unlikely that in the short term, the OPEC countries will end their use of the U.S. dollar. But, should the U.S. dollar continue the long decline outlined earlier in this article, there will be increasing incentives to diversify away and into other “stores of value” such as the euro. The consequences for the U.S. would be very serious.

4. Quantitative Easing – Dirty Deeds Done Dirt Cheap[19]

The long decline of the U.S. dollar documented earlier – a decline that is ongoing – is one reflection of the growing relative weakness of the U.S. in the context of the world economy as a whole. This growing weakness was revealed by the harsh impact of the most recent recession on the U.S. economy, one felt much more strongly there than in the other major economies. In the face of this deepest recession in a generation, the fourth and final aspect of U.S.-based currency wars came to the fore. It is without doubt the strangest of any that we have looked at, not the least because of its mysterious name, “Quantitative Easing.”

There are several ways of defining Quantitative Easing. According to the Central Bank of the United Kingdom, it is a way of injecting money into the economy “by purchasing financial assets from the private sector.” How are these assets paid for? Why “with new central bank money.” But where does that money come from? Well, “the Bank can create new money electronically by increasing the balance on a reserve account.”[20] And that’s it. New money is just simply, created. If your balance is $1,000, add a “zero” and it’s $10,000, new money created “electronically by increasing the balance on a reserve account.” Quantitative easing’s “effect is the same as printing money in vast quantities, but without ever turning on the printing presses.”[21] A skeptic would argue that the obscure term “Quantitative Easing” was chosen as less likely to arouse suspicion than a more transparent name such as “Harry Potter money creation.”

When this was policy in Japan in the wake of the deep recession of the early 1990s, it was derided in the U.S. press as something “which essentially stuffed Japanese banks with cash to help them write off huge bad loans accumulated during the 1990’s.”[22] But since 2008, this policy of creating money from nothing has been embraced with passion in the United States. In 2008, the U.S. central bank (the Federal Reserve) “bought $1.7 trillion -worth of Treasury and mortgage bonds with newly created money.”[23] That $1.7 trillion did not exist. It was brought into existence electronically, transferred to the books of financial institutions, in the hopes of pushing that newly minted money into the economy and stimulating growth. That program is now over. There is, however, every prospect that another round of Quantitative Easing will be announced in the coming weeks, with anywhere from $1 trillion to $2 trillion being created electronically to “stuff U.S. banks with cash to help them write off huge bad loans” accumulated in the last 10 years, to paraphrase the sarcastic analysis of Japan’s similar policies.

Whether or not this will stimulate growth is a matter for debate. There are, however, two things we know it will accomplish. First, it will in the long term, accelerate the decline of the U.S. dollar relative to other currencies. Second, as this flood of money depresses interest rates in the U.S., it will put upward pressure on other currencies “as investors rush elsewhere, especially into emerging economies, in search of higher yields.”[24]

Several conclusions need to be drawn here. First and most importantly, there are absolutely no grounds for Timothy Geithner or any other U.S. official to point the finger elsewhere – at China for instance – and try to fix blame for the initiation of currency wars. From blocking the creation of ICUs at Bretton Woods in 1944, to the Nixon Shock of 1971, to the Petrodollar era from 1974 to the present, the United States has demonstrated an unprecedented willingness to intervene in and artificially skew the world’s money markets. With its adoption of Quantitative Easing, it has taken this to a new level, a “shock and awe” approach to the currency wars that makes any actions by China pale in comparison.

Second, the issue of monetary policy cannot be looked at from a strictly economic point of view, but has to be examined with one eye on the economy and the other on politics. The entire economic history of the U.S. dollar is incomprehensible without the political history of U.S. imperialism. The deep distortions in the international monetary system are a reflection of the “privileges of empire” abused by the United States. The decline of that empire and the slow ending of those privileges promise to make the United States pay dearly for these distortions, but only after having wreaked havoc on much of the rest of the world.

But there is another conclusion that needs to be taken seriously, and it is something that can only be broached in this article. Conservative analysts see the history outlined above, and long nostalgically for a return to the gold standard. This is a reactionary and impossible utopia. There are just over 30,000 tonnes of gold held in official reserves around the world.[25] But even at the current high rate of $1250 an ounce, the total value of these reserves would be just over $1 trillion. The world economy is measured in tens of trillions of dollars. Any attempt to anchor the transactions of the world economy to the inflexible and slow-growing physical accumulation of gold that exists in the world would be impossible. A gold standard can simply not allow for the reflection of value in the money supply that is necessary for a modern economy to function.

However, there is an important problem, suggested by the picture sketched out here, that needs to be addressed. The break from the gold standard towards the U.S. dollar, the musing in the 1940s about an ICU, the Harry Potter economics behind quantitative easing – all are the chaotic expressions of attempts to address a very real issue. The value of the goods and services produced in the world need to be measured, reflected abstractly in some unit of measurement, and then that information used to determine investment, production and consumption decisions. The problem is not the attempt at addressing this issue. The problem is, that in a world capitalist system, this attempt is corrupted by private greed, imperialist domination of the Global South, and the militarized designs of the hegemonic state, which means that instead of a reasoned and thought-out approach, we get the dangerous chaos and instability outlined here.

Analytically, this demands taking the issue of money very seriously in anti-capitalist analysis. Marx’s brief comments on it 150 years ago are interesting. Earlier, this article used his term “world money” – money set aside for transactions between national economies in the context of the world economy. Marx argued that it is only here, “in the markets of the world that money acquires to the full extent the character of the commodity whose bodily form is also the immediate social incarnation of human labour in the abstract. Its real mode of existence in this sphere adequately corresponds to its ideal concept.”[26] The emergence of world money under capitalism takes a distorted, fetishized form. But it nonetheless represents something real – a reaching towards an adequate mechanism by which to measure the products of our labour, and redistribute them.

This process is controlled by bankers, industrialists, generals and politicians. Until it is brought under the democratic control of the vast majority – the workers in workplaces, fields and homes who produce all the wealth of the system – this money-form of capital will control us, and throw us into periodic crises which wreck economies and lives.

© 2010 Paul Kellogg. This work is licensed under a CC BY 4.0 license.

Next

“Another G20 Summit: The New Club of Hostile Brothers”

“Message to the U.S. – Blame the wars, not China”

Publishing History

This article was published as “Currency wars and the privilege of empire,” Links, 23 October.

References

[1] Gennady Sheyner. “Secretary Geithner vows not to devalue dollar.” Palo Alto Online News. 18 October, 2010.

[2] Andrew Clark. “US politicians threaten trade war with China.” guardian.co.uk. 29 September, 2010.

[3] John Maynard Keynes. The Economic Consequences of the Peace. Charleston, SC: BiblioLife, 1995 (first published 1919). Also available online.

[4] Manfred B. Steger. Globalization: A Very Short Introduction. New York: Oxford University Press, 2009: 39.

[5] George Monbiot. “Clearing Up This Mess.” Monbiot.com. 18 November, 2008.

[6] IMF. “Currency Composition of Official Foreign Exchange Reserves (COFER).” www.imf.org. 30 September, 2010. Accessed 19 October, 2010.

[7] Prior to 1999, the euro did not exist, so figures here for 1995 through to 1998 are for a “euro equivalent” – the sum of the old Deutsche mark, the French franc, the Netherlands guilder and the European Currency Unit (ECU), all of which have ceased to exist with the launch of the euro.

[8] IMF. “Currency Composition of Official Foreign Exchange Reserves (COFER).” www.imf.org. 30 September, 2010. Accessed 19 October, 2010.

[9] The concept of “World Money” (sometimes translated as “Universal Money” or “Money of the world”) was developed by Karl Marx in the first volume of Capital (Karl Marx. Capital, Volume I. In Karl Marx and Frederick Engels. Collected Works, Volume 35. New York: International Publishers, 1996: 153-156. Available online). The importance of this concept has been underlined in the contemporary period by David McNally in “From Financial Crisis to World Slump: Accumulation, Financialization, and the Global Slowdown.” 2008.

[10] Cited in Bruce Muirhead. “From Special Relationship to Third Option: Canada, the U.S., and the Nixon Shock.” American Review of Canadian Studies, 34:3, Autumn 2004: 439.

[11] “The Economy: Changing the World’s Money.” Time. 4 October, 1971.

[12] See Paul Kellogg. “The Septembers of Neoliberalism.” PolEcon.net, 29 September, 2008.

[13] Derived from Oanda.com. Accessed 19 October, 2010.

[14] Bessma Momani. “Gulf Cooperation Council Oil Exporters and the Future of the Dollar.” New Political Economy, Vol. 13, No. 3, September 2008: 297.

[15] Momani: 293.

[16] Johannes Wiegand, “Bank Recycling of Petro Dollars to Emerging Market Economies During the Current Oil Price Boom.” IMF Working Paper WP/08/180. July 2008: 4.

[17] David E. Spiro. The Hidden Hand of American Hegemony: Petrodollar Recycling and International Markets. New York: Cornell University Press, 1999: 1.

[18] Saleh M. Nsouli. “Petrodollar Recycling And Global Imbalances.” www.imf.org. 23-24 March, 2006.

[19] Apologies to AC/DC. “Dirty Deeds Done Dirt Cheap.” 1976.

[20] James Benford et. al. “Quantitative easing.” Quarterly Bulletin, Bank of England, 2009 Q2: 91.

[21] “Quantitative Easing.” The New York Times. 21 October, 2010.

[22] Martin Fackler. “Economists Are Watchful as Tokyo Ends Loose-Money Policy.” The New York Times. 9 March, 2006.

[23] “It’s all up to the Fed.” The Economist. 14 October, 2010.

[24] “How to stop a currency war.” The Economist. 14 October, 2010.

[25] World Gold Council. “World Official Gold Holdings.” September 2010.

[26] Marx: 153.

Great great summary of the historical currency war conducted by the U.S. since Bretton Woods. A few years ago I wrote a paper that boldly concluded that the Euro would become the World's new reserve currency. That conclusion, it seems, is absorbing a standing 8count. Or at least it's on the ropes with Tyson swinging away.

My view of the entire matter is from a Realist perspective and I certainly do not think some Marxist solution is an answer. I'm certainly no far right tea bagger but one has to admit that the moved by both Nixon and Dubya Bush to perpetuate and maintain U.S. dollar hegemony were clever…Did I just use Bush and clever in the same sentence? In any case,great work on this material..

High Regards

Anthony

Thanks for your reply – I'm about half-way through Wealth and Democracy by Kevin Phillips. It seems to be filling in some of the gaps in my knowledge – certainly I hadn't understood that the roots of American capitalism lie in the failed empires of the Spanish, the Dutch, and the British. Now, if I can just wrap my mind around fractional reserve banking, though in the larger scheme of things, I don't think that it matters a whole lot. Greed and avarice will find ways to express themselves.

The point you make is very relevant. The section of the article you cite is a very "condensed" statement for what has to be a much longer analysis. There is the issue of a timeline for the development of capitalism, as you indicate. Then within that timeline, there is a question of "changing focus."

The horrors of World War I and World War II are well-known. But they were not new. They were repeats of horrors committed by European and North American imperialism as it spread through the world – in Africa, the Americas and elsewhere. But, with the whole world conquered, the 20th century saw these methods "turn inward." World War II was in large measure a case of using the methods of European colonialism, but instead of in a far-away continent, focusing in on Europe.

Hitler, for instance, was a great admirer of the British empire and its conquest and domination of the Indian sub-continent. He consciously had this in mind as a model for his attempted conquest and domination of Eastern Europe and European Russia.

"Prior to 1914, capitalism had by and large been able to develop through exporting its horrors to the Global South – bringing genocide, slavery and the destruction of ancient civilizations to the Americas, Africa and Asia."

I liked your article, but I'm sufficiently uneducated (despite having a B.A. in anthropology) to "get" the timeline of the development of capitalism. Maybe one day you'll write another article that provides more detail to support the quoted sentence.

good summary.